Finance Act 2022 - Summary

Hello, Friends today we are sharing with you the Finance Act 2022 PDF to help you. If you are searching Finance Act 2022 in PDF format then you have arrived at the right website and you can directly download it from the link given at the bottom of this page. In this PDF you can check the recent change in Finance Act.

The government of India has made every change in the Finance Act from its Budget present in the parliament and you can check the New Finance Act 2022. Ministry of Law & Justice, Govt. of India has notified the Finance Act 2022, post assent/ approval of the Hon’ble President of India on 30/03/2022, in respect of the Budget Proposals (2022) for financial and direct/ indirect taxation issues, relating to FY 2022-23/ AY 2023-24.

Finance Act 2022 – Highlights Change in Finance Bill 2022

- Unexplained cash credit | Source of source: The Finance Bill has proposed an amendment to section 68 of the IT Act (section 68 deals with the taxability of “cash credits”, ie amounts received by a taxpayer for which satisfactory explanation cannot be offered by the taxpayer) to increase the burden on taxpayers from not only providing a satisfactory explanation about its source (ie the person from whom it received money), but also providing a satisfactory explanation about the “source of such source”.

- Cryptocurrencies | Virtual Digital Assets (“VDAs”): One important highlight of the Finance Bill is the proposal to introduce a separate regime for taxation of VDAs, in terms of which: (i) gains arising from the transfer of VDAs will be taxable at a flat rate of 30% (plus applicable surcharge, cess) with no set-off of any loss or cost, except the cost of acquisition of such VDA, (ii) receipt of VDAs for nil or inadequate consideration will be taxable as ordinary income in the hands of the recipient, and (iii) payments made in relation to transfer of VDAs will be subject to TDS of 1% of such consideration above specified monetary thresholds.

- Introduction of “Updated Tax Return” concept: The government is introducing a new concept of “Updated Return” to provide extra time (over and above the period that is already available under the IT Act for belated return / revised return) to taxpayers to furnish an “Updated Return” at any time within 3 years from the end of the relevant financial year (ie 2 years from the end of relevant assessment year).

- Measure to reduce departmental appeals in income-tax matters: In continuation of the government’s litigation management efforts (ie to become a non-adversarial tax regime) the Finance Bill has proposed that where a “question of law” is pending before the Supreme Court or before the jurisdictional High Court (“Pending QOL”), then, the income-tax department will not be able to file an appeal in the case of the same taxpayer or some other taxpayer until the Pending QOL is decided by the Supreme Court / jurisdictional High Court.

- Income Tax Rate: No change in the basic rate, Surcharge on Long Term Capital Gain Capped @15%

- The department not to file a further appeal to ITAT or High Court, pending the outcome on identical matters, which are sub-judice.

You can download the Finance Act 2022 PDF using the link given below.

-

Finance Act Bill 2019

Finance Act Bill 2019

-

The Finance Bill Act 2021

The Finance Bill Act 2021

-

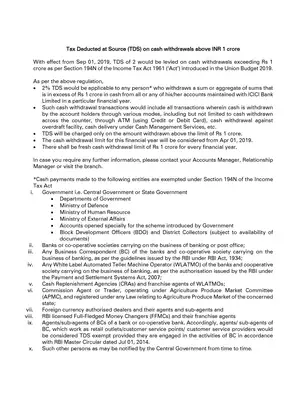

Section 194N Income Tax Act

Section 194N Income Tax Act

-

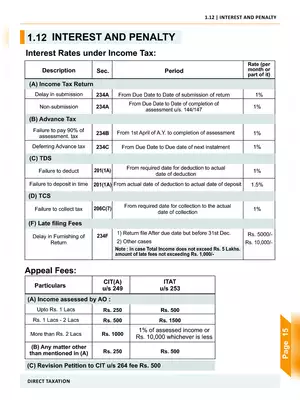

Interest & Penalty Under Income Tax Act

Interest & Penalty Under Income Tax Act

-

Vishesh Microfinance Yojana (VMY) For Disabled Persons

Vishesh Microfinance Yojana (VMY) For Disabled Persons

-

Income Tax Act 1961

Income Tax Act 1961

-

Finance Bill 2023

Finance Bill 2023

-

Finance Bill 2022

Finance Bill 2022