Credit Guarantee Scheme for Subordinate Debt (CGSSD) – Guidelines - Summary

The Scheme is named as ‘Distressed Assets Fund – Subordinate Debt for Stressed MSMEs’ and the credit product for which guarantee would be provided under the Scheme shall be named as ‘Credit Guarantee Scheme for Subordinate Debt (CGSSD)’(hereinafter referred as the ‘Scheme’)

To provide guarantee coverage for the CGSSD to provide Sub-Debt support in respect of the restructuring of MSMEs. 90% guarantee coverage would come from scheme/ Trust and the remaining 10% from the concerned promoter(s). The objective of the scheme is to provide personal loan through banks to the promoters of stressed MSMEs for infusion as equity / quasi-equity in the business eligible for restructuring, as per RBI guidelines for restructuring

of stressed MSME advances.

For the purposes of this Scheme –

- “Trust” means the Credit Guarantee Fund Trust for Micro and Small Enterprises set up by Government of India and SIDBI with the purpose of guaranteeing credit facility(ies), extended by the Member Lending Institution to the eligible borrowers.

- “Distressed Assets Fund” means a fund of Rs 4000 crore created by the Government of India for providing guarantee coverage to the loans given/ credit extended to the promoters of the eligible MSME units under the scheme.

- “Amount in Default” means the principal and interest amount outstanding in the account(s) of the borrower in respect of Sub-debt facility as on the date of the account becoming NPA, or the date of lodgment of claim application whichever is lower for preferring any claim against the guarantee cover subject to a maximum of amount guaranteed.

- “Credit facility” means financial assistance provided under the scheme by way of sub-debt facility extended by the lending institution to the Promoters of the MSME units upto 15% of promoter’s stake or Rs. 75 lakh whichever is lower. This personal loan shall not exceed the original debt of the beneficiary. Further, the Equity shall be calculated on the basis of the last available audited balance sheet of a Financial Year

- “Eligible borrower” means the promoters of MSME units which are stressed, viz. SMA-2, and NPA accounts as on 30.04.2020 and can become commercially viable as per the assessment of the lending institutions. The Scheme is applicable for those MSMEs whose accounts have been standard as on 31.03.2018 and have been in regular operations, either as standard accounts, or as NPA accounts during financial year 2018-19 and financial year 2019-20. However, fraud accounts and willful defaulters will not be considered under the proposed scheme. In cases where recovery proceedings are underway and banks assess that with the facilities provided under the scheme the account would be viable, the banks shall withdraw the recovery proceedings before going ahead with restructuring etc

- ‘Guarantee Cover’ means maximum cover available per eligible borrower of the amount in default in respect of the credit facility extended by the lending institution. For this scheme, 90% guarantee coverage would come from scheme/ Trust and the remaining 10% from the concerned promoter(s). The credit will be extended by MLIs as part of the scheme to the promoters of the stressed MSMEs to be infused by them in the form of equity/Quasi-equity/ Sub debt in the MSME which is commercially

viable. The guarantee cover would be an uncapped, unconditional, and irrevocable credit guarantee. - “Lending institution(s)” or “Member Lending institution(s) (MLIs)” means all Scheduled Commercial Bank for the time being included in the Second Schedule to the Reserve Bank of India Act, 1934, or any other institution(s) as may be directed by the Govt. of India from time to time.

- “Non-Performing Assets” means an asset classified as a non-performing based on the instructions and guidelines issued by the Reserve Bank of India from time to time.

- “Primary Security” in respect of a credit facility shall mean the assets created out of the credit facility so extended and/or existing unencumbered assets that are directly associated with the projected business for which the credit facility has been/was been extended.

- “Interest Rate” for a lending institution means the rate so declared by that lending institution from time to time as per Reserve Bank of India guidelines based on which interest rate applicable for the loan will be determined.

- “Tenure of Guarantee Cover” means the maximum period of guarantee cover from the guarantee availment date by the lending institution, which shall run through the agreed tenure of the Sub-debt facility between borrower and lending institution basis the assessment of debt serviceability or for a maximum period of 10 years whichever is earlier.

- “Collateral security” means the security provided in addition to the primary security, in connection with the credit facility extended by a lending institution to a borrower.

- “Scheme” means the ‘Distressed Asset Fund – Subordinated Debt for Stressed MSMEs scheme.

- “SIDBI” means the Small Industries Development Bank of India, established under Small Industries Development Bank of India Act, 1989 (39 of 1989).

- “Micro, Small and Medium Enterprises” as MSMEs as defined in the MSMED Act, as amended from time to time.

- Existing stake means the total contribution of the Promoter in the form of equity as well as debt. The detailed operational guidelines on the matter will be shared with MLIs of the scheme.

- “Senior Debt” means main debt already availed by the MSME that takes priority over other debt / unsecured debt owed by the issuer. The seniority status of any debt raised subsequent to implementation of the scheme will be governed by the guidelines issued by Reserve Bank of India from time to time.

- “Subordinated Debt” means a credit facility extended to the Promoter(s) of the Stressed Units for infusion in the units as Equity including Quasi Equity/Sub-Debt.

- “Stressed MSME Unit’’ means MSME Units which are stressed, viz. SMA-2 and NPA account as on 30.04.2020 as per the guidelines issued by the Reserve Bank of India from time to time.

-

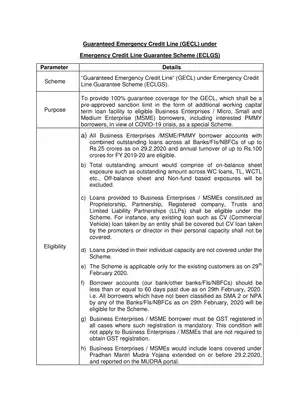

Emergency Credit Line Guarantee Scheme (ECLGS)

Emergency Credit Line Guarantee Scheme (ECLGS)

-

Pashu Kisan Credit Card (PKCC) Scheme Guidelines Hindi

Pashu Kisan Credit Card (PKCC) Scheme Guidelines Hindi

-

View Tax Credit Statement (Form 26AS) Procedure

View Tax Credit Statement (Form 26AS) Procedure

-

West Bengal Bhabishyat Credit Card Scheme

West Bengal Bhabishyat Credit Card Scheme

-

MSME Schemes List

MSME Schemes List

-

Aatmanirbhar Bharat Package / Initiatives for MSME’s

Aatmanirbhar Bharat Package / Initiatives for MSME’s

-

Atma Nirbhar Bharat Package Progress so Far

Atma Nirbhar Bharat Package Progress so Far

-

Aatma Nirbhar Bharat Abhiyan (आत्मनिर्भर भारत अभियान) Complete Details

Aatma Nirbhar Bharat Abhiyan (आत्मनिर्भर भारत अभियान) Complete Details