TDS Rate Chart FY 2022-23 - Summary

Hello, Friends today we are sharing with TDS Rate Chart FY 2022-23 PDF to help taxpayers. IF you are searching TDS Rate Chart FY 2022-23 (AY 2023-24) in PDF format then you have arrived at the right website and you can directly download the TDS Rate Chart For Ay 2023-24 PDF from the link given at the bottom of this page.

TDS or tax deducted at source is a process of collecting Income Tax at source by the GOI (Government of India). It is a deduction of tax from the original source of income. It is essentially an indirect method of collecting the tax that combines the concepts of “pay as you earn” and “collect as it is being earned.”.

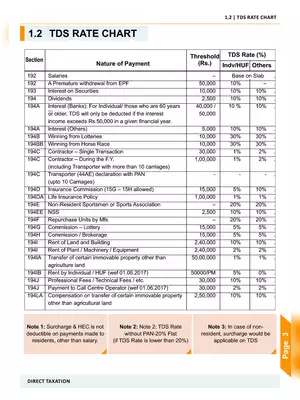

TDS Rate Chart FY 2022-23 or AY 2023-24 – TDS Section List

| Section | Nature of Payment | Threshold | TDS Rate | Remarks |

|---|---|---|---|---|

| 192 | Salary | Taxable Income liable to Tax | Normal Slab Rate (or) New Tax Regime Slab Rate as opted by the employee | Refer to Note 1 for Slab Rates |

| 192A | Payment of the accumulated balance of provident fund which is taxable in the hands of an employee. | 50,000 | 10% | – |

| 193 | Interest on securities | 2,500 | 10% | – |

| 194 | Dividend | 5,000 | 10% | – |

| 194A | Interest on Bank Deposit/Post Office Deposit/Banking Co-Society Deposit (Interest other than “Interest on securities” ) | – | ||

| a) Senior Citizen | 50,000 | 10% | – | |

| b) Others | 40,000 | 10% | – | |

| 194A | Interest other than “Interest on securities” (Other Than Bank Deposit/Post Office Deposit/Banking Co-Society Deposit) | 5,000 | 10% | – |

| 194B | Winnings from lotteries, crossword puzzles, card games and other games of any sort | 10,000 | 30% | – |

| 194BB | Winnings from horse races | 10,000 | 30% | – |

| 194C | Payment to contractor/sub-contractor: | Single Transaction: 30,000 & Aggregate of Transactions: 1,00,000 | – | |

| a) HUF/Individuals | 1% | – | ||

| b) Others | 2% | – | ||

| 194D | Insurance commission | |||

| a) Individuals | 15,000 | 5% | – | |

| b) Companies | 15,000 | 10% | – | |

| 194DA | Payment in respect of life insurance policy, the tax shall be deducted on the amount of income comprised in insurance pay-out | 1,00,000 | 5% | – |

| 194E | Payment to non-resident sportsmen/sports association | – | 20% | The rate of TDS shall be increased by applicable surcharge and Health & Education cess. |

| 194EE | Payment in respect of deposit under National Savings scheme | 2,500 | 10% | – |

| 194F | Payment on account of repurchase of unit by Mutual Fund or Unit Trust of India | – | 20% | – |

| 194G | Commission on sale of lottery tickets | 15,000 | 5% | – |

| 194H | Commission or brokerage | 15,000 | 5% | – |

| 194-I | Rent: | |||

| 194-I(a) Plant & Machinery | 2,40,000 | 2% | – | |

| 194-I(b) Land or building or furniture or fitting | 2,40,000 | 10% | – | |

| 194-IA | Payment on transfer of certain immovable property other than agricultural land | 50 Lakh | 1% | Budget 2022 Update |

| 194-IB | Payment of rent by individual or HUF not liable to tax audit | 50,000 per month | 5% | – |

| 194-IC | Payment of monetary consideration under Joint Development Agreements | – | 10% | – |

| 194J | Fees for professional or technical services: | |||

| i) sum paid or payable towards fees for technical services | 30,000 | 2% | – | |

| ii) sum paid or payable towards royalty in the nature of consideration for sale, distribution or exhibition of cinematographic films; | 30,000 | 2% | – | |

| iii) Any other sum | 30,000 | 10% | – | |

| 194K | Income in respect of units payable to resident person | – | 10% | – |

| 194LA | Payment of compensation on acquisition of certain immovable property | 2,50,000 | 10% | – |

| 194LB | Payment of interest on infrastructure debt fund to Non Resident | – | 5% | The rate of TDS shall be increased by applicable surcharge and Health & Education cess. |

| 194LBA(1) | A business trust shall deduct tax while distributing, any interest received or receivable by it from an SPV or any income received from renting or leasing or letting out any real estate asset owned directly by it, to its unitholders. | – | 10% | – |

| 194LBB | Investment fund paying an income to a unitholder [other than income which is exempt under Section 10(23FBB)] | – | 10% | – |

| 194LBC | Income in respect of investment made in a securitization trust (specified in Explanation of section115TCA) | |||

| a) HUF/Individuals | – | 25% | – | |

| b) Others | – | 30% | – | |

| 194M | Payment of commission (not being insurance commission), brokerage, contractual fee, professional fee to a resident person by an individual or a HUF who are not liable to deduct TDS under section 194C, 194H, or 194J. | 50 Lakh | 5% | – |

| 194N | Cash withdrawal during the previous year from one or more accounts maintained by a person with a banking company, cooperative society engaged in the business of banking or a post office: | |||

| i) in excess of Rs. 1 crore | 1 Crore | 2% | – | |

| ii) in excess of Rs. 20 lakhs (for those persons who have not filed return of income (ITR) for three previous years immediately preceding the previous year in which cash is withdrawn, and the due date for filing ITR under section 139(1) has expired.) The deduction of tax under this situation shall be at the rate of: | ||||

| a) On amount withdrawn in cash if the aggregate of the amount of withdrawal exceeds Rs. 20 lakhs during the previous year; | 20 Lakh | 2% | – | |

| b) On amount withdrawn in cash if the aggregate of the amount of withdrawal exceeds Rs. 1 crore during the previous year; | 1 Crore | 5% | – | |

| 194-O | Payment or credit of amount by the e-commerce operator to e-commerce participant | 5 Lakh | 1% | In case of non-availability of PAN, TDS Rate shall be 5% |

| 194Q | Purchase of goods (applicable w.e.f 01.07.2021) | 50 Lakh | 0.10% | – |

| 195 | Payment of any other sum to a Non-resident | The rate of TDS shall be increased by applicable surcharge and Health & Education cess. | ||

| a) Income in respect of investment made by a Non-resident Indian Citizen | – | 20% | – | |

| b) Income by way of long-term capital gains referred to in Section 115E in case of a Non-resident Indian Citizen | – | 10% | – | |

| c) Income by way of long-term capital gains referred to in sub-clause (iii) of clause (c) of sub-Section (1) of Section 112 | – | 10% | – | |

| d) Income by way of long-term capital gains as referred to in Section 112A | – | 10% | – | |

| e) Income by way of short-term capital gains referred to in Section 111A | – | 15% | – | |

| f) Any other income by way of long-term capital gains [not being long-term capital gains referred to in clauses 10(33), 10(36) and 112A | – | 20% | – | |

| g) Income by way of interest payable by the Government or an Indian concern on moneys borrowed or debt incurred by the Government or the Indian concern in foreign currency (not being income by way of interest referred to in Section 194LB or Section 194LC) | – | 20% | – | |

| h) Any other Income | – | 30% | – | |

| 194P | TDS on Senior Citizen above 75 Years | Taxable Income liable to Tax | Tax Rates in Force | Refer to Note 1 for Slab Rates |

| 206AB | TDS on non-filers of ITR at higher rates | Refer Note 3 | Higher of the followings rates –

| Budget 2022 Update |

| 206AA | TDS rate in case of Nonavailability of PAN | As per the respective section | Tax shall be deducted at the higher of the following rates, namely:— (i) at the rate specified in the relevant provision of this Act; or (ii) at the rate or rates in force; or (iii) at the rate of 20% | – |

| 194R | TDS on benefit or perquisite of a business or profession | 20,000 | 10% | Introduced in Budget 2022 |

| 194S | TDS on payment for Virtual Digital Assets | “Specified Person” Payer– 50,000 Other Payers – 10,000 | 1% | Introduced in Budget 2022 |

Income Tax Basic Salb Rate FY 2022-23 (AY 2023-24)

| Net Income Range | Rate of Income Tax |

|---|---|

| 1.1 Individuals (Other than senior and super senior citizens) | |

| Up to Rs. 2,50,000 | – |

| Rs. 2,50,000 to Rs. 5,00,000 | 5% |

| Rs. 5,00,000 to Rs. 10,00,000 | 20% |

| Above Rs. 10,00,000 | 30% |

| 1.2 Individuals (Senior Citizen) | |

| Up to Rs. 3,00,000 | – |

| Rs. 3,00,000 to Rs. 5,00,000 | 5% |

| Rs. 5,00,000 to Rs. 10,00,000 | 20% |

| Above Rs. 10,00,000 | 30% |

| 1.3 Individuals (Super Senior Citizen) | |

| Up to Rs. 5,00,000 | – |

| Rs. 5,00,000 to Rs. 10,00,000 | 20% |

| Above Rs. 10,00,000 | 30% |

New Tax Regime Slab Rate for Ay 2023-24

The Finance Act, 2020, has provided an option to Individuals and HUF for payment of taxes at the following reduced rates from Assessment Year 2021-22 and onwards:-

| Total Income (Rs) | Rate |

|---|---|

| Up to 2,50,000 | Nil |

| From 2,50,001 to 5,00,000 | 5% |

| From 5,00,001 to 7,50,000 | 10% |

| From 7,50,001 to 10,00,000 | 15% |

| From 10,00,001 to 12,50,000 | 20% |

| From 12,50,001 to 15,00,000 | 25% |

| Above 15,00,000 | 30% |

You can download the TDS Rate Chart FY 2022-23 PDF using the link given below.

-

TDS Rate Chart FY 2023-24

TDS Rate Chart FY 2023-24

-

TDS Rates Chart for FY 2021-22 or AY 2022-23

TDS Rates Chart for FY 2021-22 or AY 2022-23

-

TDS & TCS Slab Rate for AY 2020-21

TDS & TCS Slab Rate for AY 2020-21

-

TDS/TSC New/Revised Rates Chart AY 2021-22

TDS/TSC New/Revised Rates Chart AY 2021-22

-

TDS/TCS Rate Chart for AY 2020-21

TDS/TCS Rate Chart for AY 2020-21

-

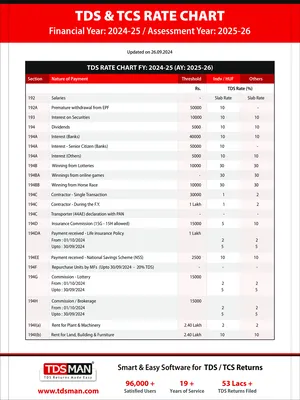

TDS Section List 2024-25 (AY 2025-26)

TDS Section List 2024-25 (AY 2025-26)

-

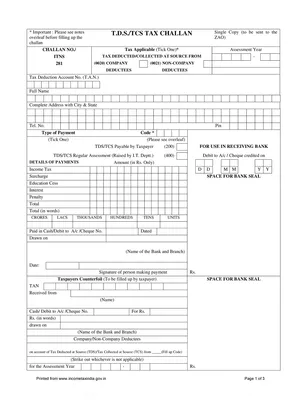

TDS/TCS Tax Challan Form 281

TDS/TCS Tax Challan Form 281

-

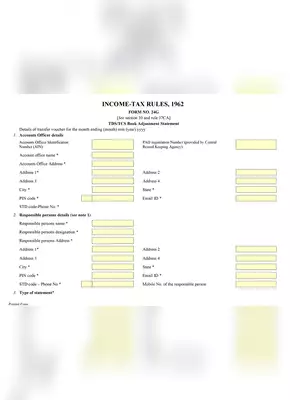

Form No 24G – TDS/TCS Book Adjustment Statement

Form No 24G – TDS/TCS Book Adjustment Statement