TDS Rates Chart for FY 2021-22 or AY 2022-23 - Summary

TDS is deducted as per the Indian Income Tax Act, 1961. IT is controlled by the Central Board for Direct Taxes, and it is a part of the Indian Revenue Service Department. Tax Deduction at Source (TDS) is one of the important compliance for Income Tax Assessee. Every Deductor has to deduct the TDS at the specified rate, if the payment exceeds the threshold limit specified in the particular section. There are various sections in Income Tax Law, which specify different TDS rates, nature of payment & its threshold limits for TDS

TDS or tax deducted at source is a process of collecting Income Tax at source by the GOI (Government of India). It is a deduction of tax from the original source of income. It is essentially an indirect method of collecting tax which combines the concepts of “pay as you earn” and “collect as it is being earned.”

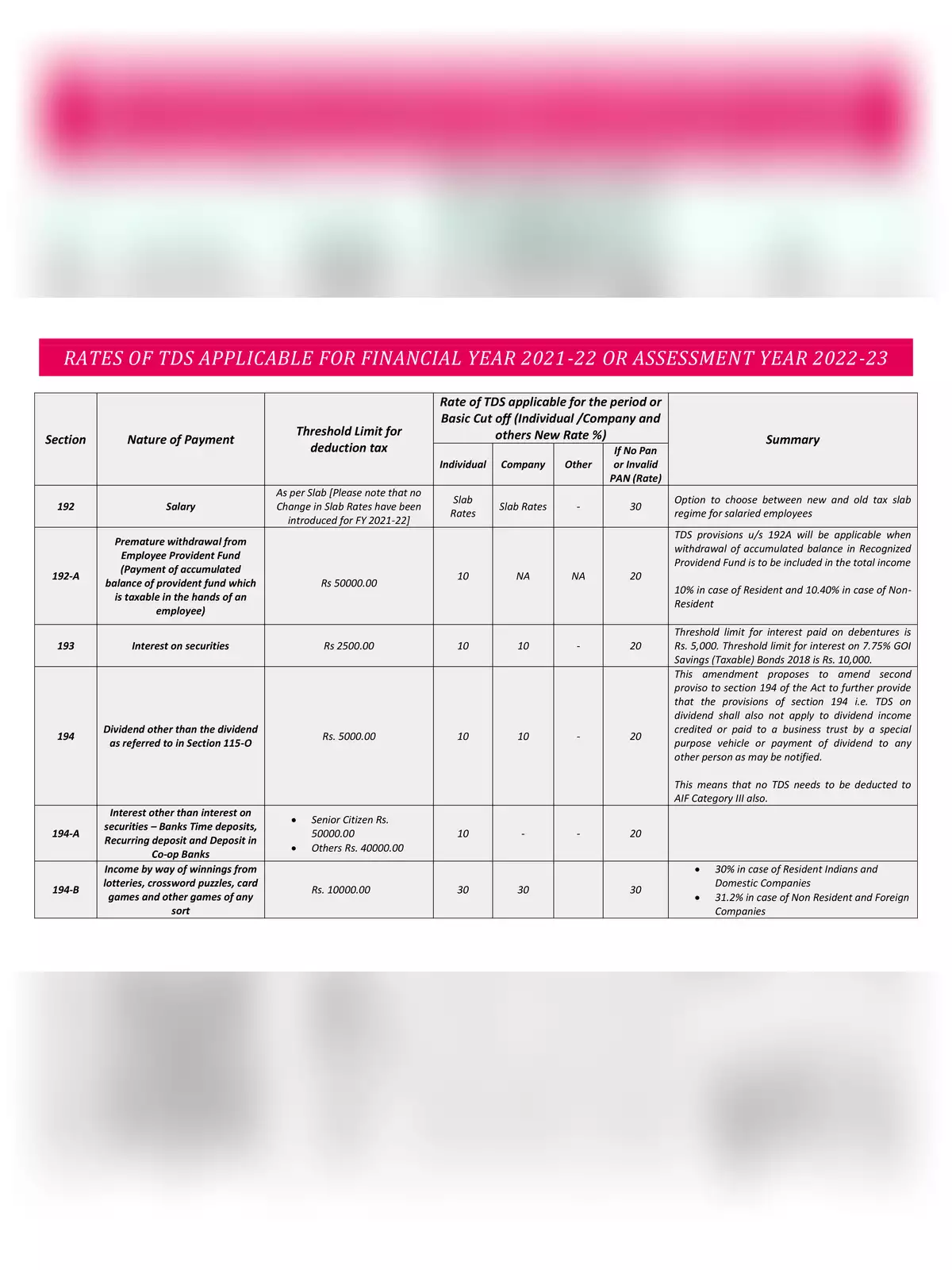

Here is the TDS Chart for FY 2021-22 or AY 2022-23

| Nature of Payment | Basic Cut off (Rs.) | Individual /Company and others New Rate %) | If No Pan or Invalid PAN (Rate %) |

| 192 – Salaries | Slab Rate | Slab Rates | 30% |

| 192A- Premature withdrawal from Employee Provident Fund (Note 1) | 50,000 | Individual: 10% Company: NA | 20% |

| 193 – Interest on securities (Note 2) | 2,500 | Individual: 10% Company: 10%` | 20% |

| 194 – Dividend other than the dividend as referred to in Section 115-O | 5,000 | Individual: 10% Company: 10% | 20% |

| 194A – Interest other than interest on securities – Banks Time deposits, Recurring deposit and Deposit in Co-op Banks (Note 3) | 40,000 (for individual) 50000 (for Senior Citizens) | Individual: 10% | 20% |

| 194B – Winning from Lotteries | 10,000 | Individual: 30% Company: 30% | 30% |

| 194BB – Winnings from Horse Race | 10,000 | Individual: 30% Company: 30% | 30% |

| 194C- Payment to Contractor – Single Transaction (Note 3) | 30,000 | Individual: 1% Company: 2% | 20% |

| 194C-Payment to Contractor – Aggregate During the Financial year (Note 3) | 1,00,000 | Individual: 1% Company: 2% | 20% |

| 194C- Contract – Transporter not covered under 44AE (Note 3 & 4) | 30,000 / 75,000 | Individual: 1% Company: 2% | 20% |

| 194C- Contract – Transporter covered under 44AE & submit declaration on prescribed form with PAN | – | – | 20% |

| 194D – Insurance Commission | 15,000 | Individual: 5% Company: 5% | 20% |

| 194DA Payment in respect of life insurance policy (Note 5) | 1,00,000 | Individual: 5% Company: 5% | 20% |

| 194E – Payment to Non-Resident Sportsmen or Sports Association | – | Individual: 20% Company: 20% | 20% |

| 194EE – Payments out of deposits under National Savings Scheme | 2,500 | Individual: 10% Company: 10% | 20% |

| 194F – Repurchase Units by MFs | – | Individual: 20% Company: 20% | 20% |

| 194G – Commission – Lottery | 15,000 | Individual: 5% Company: 5% | 20% |

| 194H – Commission / Brokerage (Note 3) | 15,000 | Individual: 5% Company: 5% | 20% |

| 194I – Rent – Land and Building – furniture – fittings (Note 3) | 2,40,000 | Individual: 10% Company: 10% | 20% |

| 194I – Rent – Plant / Machinery / equipment (Note 3) | 2,40,000 | Individual: 2% Company: 2% | 20% |

| 194IA -Transfer of certain immovable property other than agriculture land | 50,00,000 | Individual: 1% Company: 1% | 20% |

| 194IB – Rent – Land or building or both | 50,000 per month | Individual: 5% | 20% |

| 194IC – Payment of Monetary consideration under Joint development agreement | – | Individual: 10% Company: 10% | 20% |

| 194J – Professional Fees for technical services (w.e.f. from 1.4.2020) (Note 3 and 6) | 30,000 | Individual: 2% Company: 2% | 20% |

| 194J – Professional Fees in all other cases (Note 3) | 30,000 | Individual: 10% Company: 10% | 20% |

| 194K- Payment of any income in respect of Units of Mutual fund as per section 10(23D) or Units of administrator or from a specified company (Note 7) | – | Individual: 10% Company: 10% | 20% |

| 194LA – TDS on compensation for compulsory acquisition of immovable Property (Note 8) | 2,50,000 | Individual: 10% Company: 10% | 20% |

| 194 LBA (1)- Business trust shall deduct tax while distributing, any interest received or receivable by it from a SPV or any income received from renting or leasing or letting out any real estate asset owned directly by it, to its unit holders. (Note 9) | Individual: 10% Company: 10% | 20% | |

| 194LB – Income by way of interest from infrastructure debt fund (non-resident) | – | Individual: 5% Company: 5% | 20% |

| 194LBB – Income in respect of investment in Securitisation trust. | – | Individual: 10% Company: 30% | 30% |

| 194LBC- Income in respect of investment made in a securitisation trust | – | Individual: 25% Company: 30% | 30% |

| 194 LC – Income by way of interest by an Indian specified company to a non-resident / foreign company on foreign currency approved loan / long-term infrastructure bonds from outside India (Note 10) | – | Individual: 5% Company: 5% | 20% |

| 194LD – Interest on certain bonds and govt. Securities (Note 11) | – | Individual: 5% Company: 5% | 20% |

| 194M – Payment of Commission, brokerage, contractual fee, professional fee to a resident person by an Individual or a HUF who are not liable to deduct TDS under section 194C, 194H, or 194J. | 50,00,000 | Individual: 5% Company: 5% | 20% |

| 194N – Cash withdrawal in excess of Rs. 20 Lakh during the previous year from one or more account maintained by a person with a banking company, co-operative society engaged in business of banking or a post office. | 20,00,000 | Individual: 2% Company: 2% | 20% |

| 194N – Cash withdrawal in excess of Rs. 1 crore during the previous year from one or more account maintained by a person with a banking company, co-operative society engaged in business of banking or a post office. (Note 12) | 100,00,000 | Individual: 2% Company: 2% | 20% |

| 194O – Applicable for E-Commerce operator for sale of goods or provision of service facilitated by it through its digital or electronic facility or platform. | – | Individual: 1% Company: 1% | 20% |

| 194P- TDS by specified bank to specified senior citizen | – | Rates applicable to particular slab of income including applicable Surcharge and Health & Education Cess | |

| 194Q- Purchase of goods | 50,00,000 | 0.10% | |

| 195- Payment of any sum to Non resident | – | – | Higher of Rate in force or Double Taxation Avoidance Act rate |

| 196B – Income from units | – | Individual: 10% Company: 10% | 20% |

| 196C-Income from foreign currency bonds or GDR (including long-term capital gains on transfer of such bonds) (not being dividend) | – | Individual: 10% Company: 10% | 20% |

| 196D – Income of FIIs from securities | – | Individual: 20% Company: 20% | 20% |

You can download the TDS Rates Chart for FY 2021-22 in PDF format using the link given below.

-

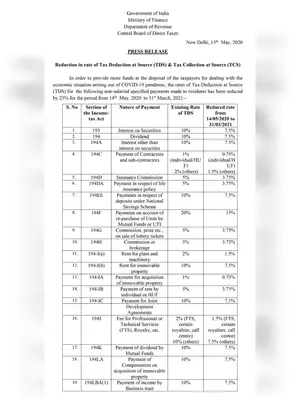

TDS/TSC New/Revised Rates Chart AY 2021-22

TDS/TSC New/Revised Rates Chart AY 2021-22

-

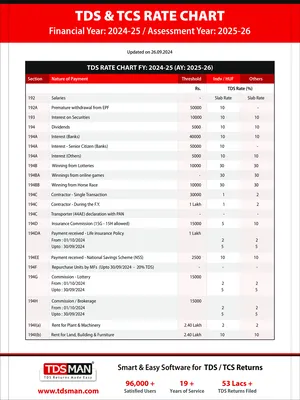

TDS Section List 2024-25 (AY 2025-26)

TDS Section List 2024-25 (AY 2025-26)

-

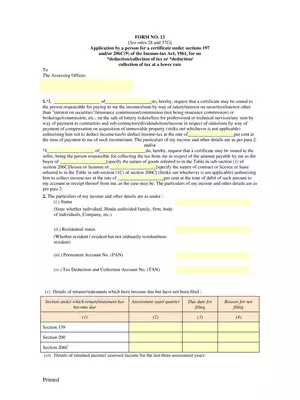

Form 13 – Non-Deduction / Lower Deduction of TDS

Form 13 – Non-Deduction / Lower Deduction of TDS

-

TDS Rate Chart FY 2023-24

TDS Rate Chart FY 2023-24

-

TDS Section List 2022-23

TDS Section List 2022-23

-

TDS Rate Chart FY 2022-23

TDS Rate Chart FY 2022-23

-

TDS & TCS Slab Rate for AY 2020-21

TDS & TCS Slab Rate for AY 2020-21

-

Income Tax Computation Format

Income Tax Computation Format