TDS Section List 2024-25 (AY 2026-26) - Summary

TDS stands for Tax Deducted at Source. It is a way the government collects tax from your income directly at the time it is earned. For example, when you receive a salary or payment, a small portion of it is taken as tax and sent to the government. This helps stop tax evasion and ensures regular income for the government.

The Income Tax Act has different sections for TDS based on the type of payment. Each section tells us how much tax to deduct and when to deduct it. Some common sections include TDS on salary, interest, rent, and contractor payments. This list of TDS sections helps people understand which rule applies to their income or business payments.

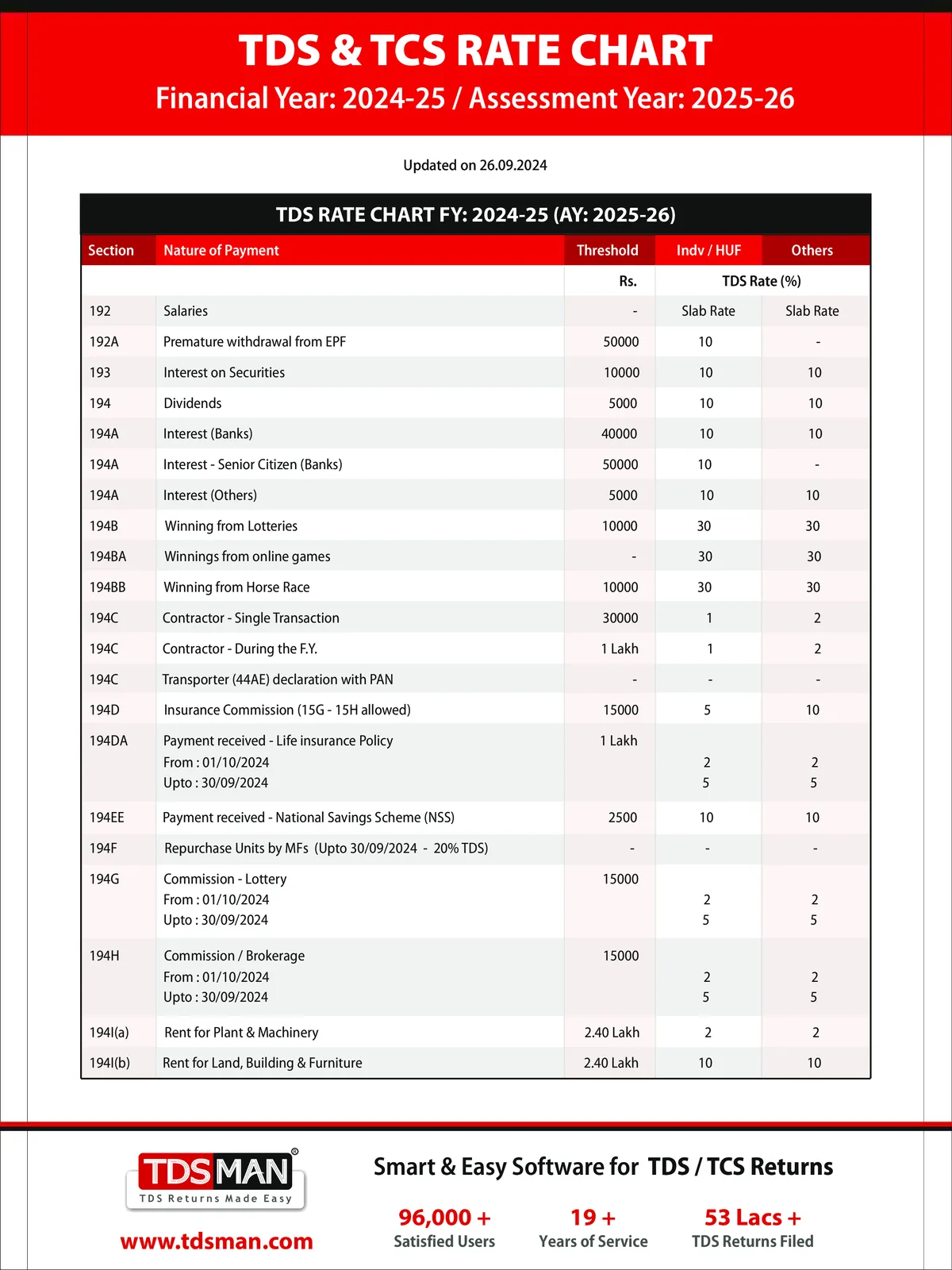

TDS Rate Chart for FY 2024-25 (AY 2025-2026)

| Section | Nature of Payment | Threshold (Rs.) | Individual / HUF TDS Rates (%) | Others TDS Rate (%) |

|---|---|---|---|---|

| 192 | Salaries | Rs. 2,50,000 | Slab Rates | Slab Rates |

| 192A | Premature EPF withdrawal* | Rs. 50,000 | 10% | 10% |

| 193 | – TDS on interest on securities*** | Rs. 10,000 | 10% | 10% |

| 194 | Payment of dividend | Rs. 5,000 | 10% | 10% |

| 194A | Interest issued by banks or post offices on deposits | Rs. 40,000 Rs. 50,000 (For senior citizens) | 10% | 10% |

| 194A | Interest by others apart from on securities | Rs. 5,000 | 10% | 10% |

| 194B | Amounts that someone has won through lotteries, puzzles, or games | Aggregate of Rs. 10,000** | 30% | 30% |

| 194BB | Amounts that someone has won from horse races | Rs. 10,000 | 30% | 30% |

| 194C | Payments to contractor or sub-contractor – Single Payments | Rs. 30,000 | 1% | 2% |

| 194C | Payments to contractor/sub-contractor – Aggregate Payments | Rs. 1,00,000 | 1% | 2% |

| 194D | Payment of insurance commission to domestic companies | Rs. 15,000 | NA | 10% |

| 194D | Payment of insurance commission to companies other than domestic ones | Rs. 15,000 | 5% | NA |

| 194DA | Maturity of Life Insurance Policy | Rs. 1,00,000 | 5% | 5% |

| 194EE | Payment of an amount standing to the credit of an individual under NSS (National Savings Scheme) | Rs. 2500 | 10% | 10% |

| 194F | Payment of repurchase of unit by UTI (Unit Trust of India) or any mutual fund | No Limit | 20% | 20% |

| 194G | Payments or commission on sale of lottery tickets | Rs. 15,000 | 5% | 5% |

| 194H | Commission or brokerage | Rs. 15,000 | 5% | 5% |

| 194I | Rent of land, building, or furniture | Rs. 2,40,000 | 10% | 10% |

| 194I | Rent of plant and machinery | Rs. 2,40,000 | 2% | 2% |

| 194IA | Payment for transfer of immovable property other than agricultural land | Rs. 50,00,000 | 1% | 1% |

| 194IB | Rent payment that is made by an individual or HUF not covered under payment 194I | Rs. 50,000 (per month) | 5% | NA |

| 194IC | Payment that are made under Joint Development Agreement (JDA) to Individual/HUF | No Limit | 10% | 10% |

| 194J | Fees paid for professional services | Rs. 30,000 | 10% | 10% |

| 194J | Amount paid for technical services | Rs. 30,000 | 2% | 2% |

| 194J | Amounts paid as royalty for sale/distribution/exhibition of cinematographic films | Rs. 30,000 | 2% | 2% |

| 194K | Payment of income for units of a mutual fund, for example- dividends | Rs. 5,000 | 10% | 10% |

| 194LA | Payment made for compensation for acquiring certain immovable property | Rs. 2,50,000 | 10% | 10% |

| 194LB | Payment of interest on infrastructure bonds to Non-Resident Indians | NA | 5% | 5% |

| 194LBA(1) | Certain income distributed by a business trust among its unit holder | NA | 10% | 10% |

| 194LD | Payment of interest on rupee-denominated bonds, municipal debt security, and government securities | NA | 5% | 5% |

| 194M | Amounts paid for contract, brokerage, commission or professional fee (other than 194C, 194H, 194J) | Rs. 50,00,000 | 5% | 5% |

| 194N | In case cash withdrawal over a certain amount takes place from the bank, and ITR is filed | Rs. 1,00,00,000 | 2% | 2% |

| 194N | In case cash withdrawal takes place from a bank and one does not file ITR | Rs. 20,00,000 | 2% | 2% |

| 194O | Amount paid for the sale of products/services by e-commerce service providers via their digital platform | Rs. 5,00,000 | 1% | 1% |

| 194Q | Payments made for the purchase of goods | Rs. 50,00,000 | 0.10% | 0.10% |

| 194S | TDS on the payment of any crypto or other virtual asset | NA | 1% | 1% |

| 206AA | TDS for non-availability of PAN | NA | At a rate higher of

| 20% |

| 206AB | TDS on non-filers of Income tax return | NA | Rate higher of:

|